Whether you’re new to the nonprofit world or just looking to brush up on your accounting knowledge, one of the first things you’ll need to understand is your organization’s Statement of Financial Position.

The Statement of Financial Position – also known as a balance sheet – shows your organization’s assets (what you own), liabilities (what you owe), and net assets (equity). This statement is a snapshot; it shows where you stand financially at a specific point in time. It does not show the flow of income or expenses over time. (For that, you’ll need to look at your Statement of Activities instead.)

Assets are things that an organization owns that have value.

Assets include cash, investments, physical property like buildings or land, equipment, and inventory. Accounts receivable – the amount owed to your organization by others – is also an asset. Assets can also include non-physical things like trademarks and patents.

Assets are categorized based on how quickly they will be converted into cash. Current assets are those that you expect to convert to cash within one year (like inventory or accounts receivable). Non-current assets are those that you do not expect to convert to cash within one year, or those that would take longer than one year to sell (like long-term investments or trademarks). Fixed assets are a type of non-current assets that are used to operate your organization but are not available for sale (like buildings, vehicles and furniture).

Liabilities are debts that an organization owes to others.

Liabilities can include all kinds of obligations, like money borrowed from a bank, accounts payable (money your organization owes to vendors), payroll that your organization owes to employees, and taxes that are owed to federal, state, and local governments.

Liabilities are generally categorized based on their due dates. Current liabilities are those you expect to pay off within the year. Long-term liabilities are those with due dates that are more than one year away.

Net Assets are the difference between assets and liabilities.

Net assets are what would remain if your organization sold all of its assets and paid off all of its liabilities. In the for-profit business world, this “leftover” money is known as equity – how much the shareholders and partners actually own after all debts are settled. Since nonprofits do not have shareholders, this section of the Statement of Financial Position is simply called “Net Assets.”

Net assets are categorized based on the existence or absence of donor restrictions. Unrestricted net assets do not have any restrictions on how your organization can use those funds. Restricted net assets come with specific donor-imposed stipulations or conditions. (For example, a donation to purchase computer equipment cannot be used to pay for staff salaries, utility costs, rent, or other supplies – those funds can only be used to purchase computers.)

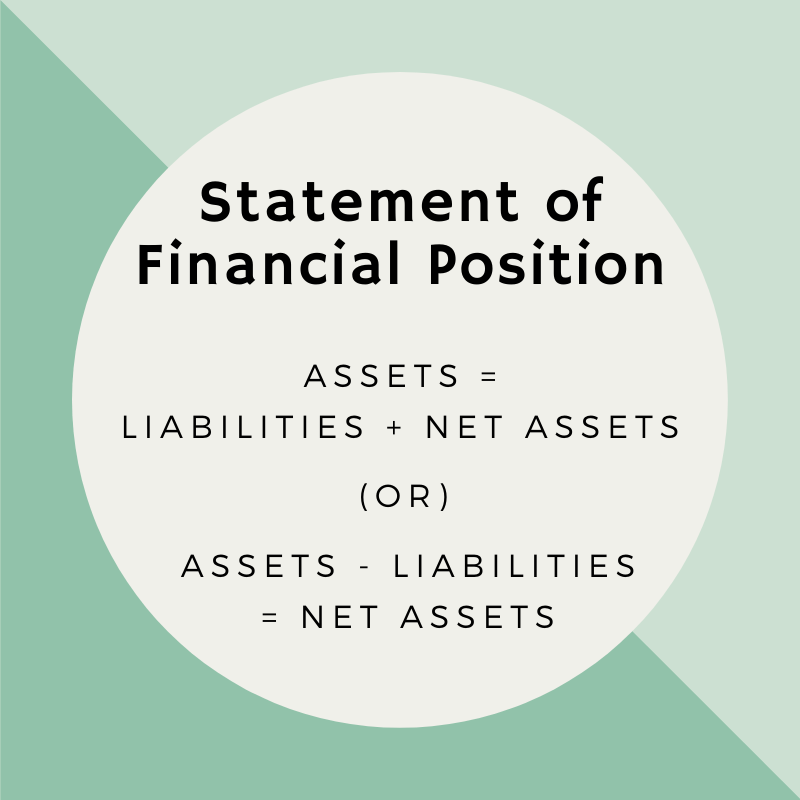

A nonprofit Statement of Financial Position ultimately comes down to a very simple equation:

Assets = Liabilities + Net Assets

Or, to rearrange the equation to make it clearer:

Assets - Liabilities = Net Assets

If you owned a house (an asset) valued at $300K, and you had an outstanding mortgage balance (a liability) of $200K, your net assets (equity) would be $100K. Likewise, your nonprofit’s net assets are the difference between your assets and liabilities. This equation should always remain in balance. If your assets increase and your liabilities stay the same, then your net assets will also increase. But if your liabilities increase without any corresponding increase in assets, then your net assets will decrease.

A nonprofit Statement of Financial Position can be difficult to interpret at first glance, but by understanding how these three components work together on this report, you can gain a better understanding of your organization’s financial health.